In the modern financial landscape, the need for quick, reliable, and transparent credit solutions has never been higher. For many consumers in Finland and the surrounding regions, the term onnilaina has become synonymous with accessible consumer credit. Whether it is for an unexpected home repair, a medical emergency, or consolidating smaller debts into a more manageable single payment, understanding how these financial products work is essential for maintaining a healthy economic life.

This article provides an in-depth exploration of the onnilaina ecosystem, covering everything from eligibility requirements and interest rates to the legal regulations that protect borrowers in the digital age.

What is Onnilaina?

At its core, onnilaina (which translates roughly from Finnish as “Luck Loan” or “Happiness Loan”) refers to a type of unsecured personal loan or consumer credit. Unlike a traditional mortgage or a car loan, an unsecured loan does not require the borrower to put up collateral, such as a house or a vehicle.1

This financial product is designed for flexibility. It fills the gap between small payday loans and large-scale bank financing. Most people seek an onnilaina when they need a sum ranging from a few hundred euros to several thousand, with repayment terms that can span from a few months to several years.

The Evolution of Digital Lending

Historically, getting a loan required a physical visit to a bank branch, multiple face-to-face meetings, and stacks of paperwork. However, the rise of fintech has transformed the industry. Today, an onnilaina application can be completed entirely online, often within minutes. This digital shift has democratized access to credit, allowing individuals in remote areas or those with busy schedules to manage their finances with a few clicks on a smartphone.2

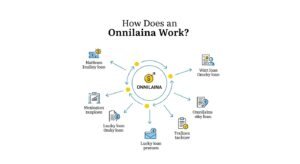

How Does an Onnilaina Work?

The mechanics of an onnilaina are straightforward, but they require careful attention to detail. When a borrower applies for this type of credit, the lender assesses their creditworthiness through automated systems.

- Application: The user fills out an online form providing personal details, income information, and the desired loan amount.

- Verification: Most lenders use strong electronic identification (such as Tunnistautuminen via bank IDs) to verify the applicant’s identity.

- The Offer: If approved, the lender provides an offer detailing the interest rate, monthly installments, and the total cost of credit.

- Payout: Once the contract is signed electronically, the funds are usually transferred to the borrower’s bank account quickly—sometimes on the same day.

The term onnilaina is often used by aggregators and brokers who help users compare different loan offers from various banks to ensure they get the most competitive rates available in the market.

Eligibility Criteria for Borrowers

Not everyone who applies for an onnilaina will be approved. Lenders have strict criteria to ensure that the borrower has the capacity to repay the debt without falling into financial distress. Common requirements include:

- Age: Usually, applicants must be at least 18 years old, though some lenders require a minimum age of 20 or 23.

- Residency: A permanent address in Finland is typically required.3

- Income: A steady source of income, whether from a salary or a pension, must be demonstrated.

- Credit History: A clean credit record is vital. In the Finnish system, having a “maksuhäiriömerkintä” (credit default entry) is almost always an automatic grounds for rejection for an onnilaina.

- Bank Account: A valid personal bank account with online banking credentials for identity verification.

Understanding the Costs: Interest and Fees

One of the most critical aspects of taking out an onnilaina is understanding that the “sticker price” isn’t the only cost involved. Borrowers must look at the Annual Percentage Rate (APR), known in Finland as todellinen vuosikorko.

Breakdown of Costs:

| Cost Component | Description |

| Nominal Interest | The base interest rate applied to the principal amount. |

| Opening Fee | A one-time fee charged when the loan is first granted. |

| Account Management Fee | A monthly recurring fee for maintaining the loan account. |

| Late Payment Fees | Charges applied if an installment is not paid by the due date. |

Since 2019, Finnish legislation has placed a strict cap on the interest rates for consumer credit like onnilaina.4 The nominal interest rate is capped at 20%, and other costs associated with the loan are also strictly regulated to prevent predatory lending practices.

The Pros and Cons of an Onnilaina

Before committing to a loan, it is wise to weigh the advantages against the potential drawbacks.

Advantages

- Speed: The primary benefit of an onnilaina is the speed of delivery. It is an ideal solution for urgent financial needs.

- No Collateral: Borrowers do not risk their assets (like their home) if they struggle with payments, although their credit score will be affected.

- Digital Convenience: Applications can be submitted 24/7 from anywhere.

- Flexibility: Funds can be used for any purpose, from home renovations to consolidating higher-interest credit card debt.

Disadvantages

- Higher Interest: Compared to secured loans (like a mortgage), an onnilaina usually carries a higher interest rate because the lender takes on more risk.

- Debt Trap Potential: The ease of access can lead some individuals to borrow more than they can afford to pay back.

- Impact on Credit: Any missed payments will negatively impact the borrower’s ability to get credit in the future.

The Importance of Loan Comparison

When looking for an onnilaina, the first offer you receive is not necessarily the best one. Different banks have different “appetites” for risk, meaning one lender might offer you a 10% interest rate while another offers 18% for the exact same amount.

Using comparison services is the most efficient way to find a cost-effective onnilaina. These platforms send your application to dozens of different banks simultaneously. This competition between lenders works in the consumer’s favor, driving down interest rates and improving the terms of the loan.

Responsible Borrowing Practices

Taking out an onnilaina is a significant financial commitment. To ensure that the loan serves as a tool for “onni” (happiness) rather than stress, follow these best practices:

1. Evaluate the Necessity

Ask yourself if the purchase is essential. If it is for a luxury item, it might be better to save up over time rather than paying interest on a loan.

2. Calculate Your Budget

Before signing an onnilaina contract, create a detailed monthly budget. Ensure that after paying your rent, groceries, and utilities, you have enough “buffer” to cover the loan installment comfortably.

3. Read the Fine Print

Never sign a contract without reading the terms and conditions. Pay special attention to the total amount repayable over the life of the loan.

4. Avoid “Loan Stacking”

Taking out a new onnilaina to pay off an old one is a dangerous cycle. If you find yourself in this position, it is better to seek financial counseling or look into debt consolidation options rather than taking on more high-interest credit.

Legal Protections for Borrowers

In Northern Europe, consumer protection laws are among the strongest in the world. When you take out an onnilaina, you are protected by the Consumer Protection Act. This includes:

- Right of Withdrawal: Borrowers usually have a 14-day window to cancel the loan agreement if they change their mind, provided they return the principal amount.

- Transparency Requirements: Lenders must clearly state the total cost of the loan and the APR in all marketing materials and contracts.

- Interest Caps: As mentioned previously, the law limits how much a lender can charge in interest and fees for an onnilaina.

These regulations ensure that the market for an onnilaina remains fair and that consumers are not exploited by hidden fees or astronomical interest rates.

Future Trends in Consumer Credit

The world of onnilaina continues to evolve. We are seeing a move toward “Open Banking,” where lenders can (with the borrower’s permission) view real-time transaction data to make faster and more accurate lending decisions.5 This could lead to even lower interest rates for those with disciplined spending habits.

Furthermore, there is an increasing focus on “Green Loans.” Some lenders may offer a lower interest rate on an onnilaina if the funds are used for environmentally friendly purposes, such as installing solar panels or improving home insulation.

Conclusion

An onnilaina can be a powerful financial tool when used correctly. It provides a safety net for life’s unexpected turns and offers a way to manage large expenses without needing years of prior saving. However, the responsibility lies with the borrower to treat credit with respect.

By comparing offers, understanding the total cost of the APR, and ensuring the monthly payments fit within a realistic budget, you can use an onnilaina to achieve your financial goals without compromising your long-term economic stability. Always remember that the best loan is one that is planned, understood, and repaid on time.

In the end, whether an onnilaina brings “onni” or hardship depends entirely on the financial literacy and discipline of the borrower. Use the digital tools at your disposal, stay informed about your rights, and always borrow with a clear plan for the future.